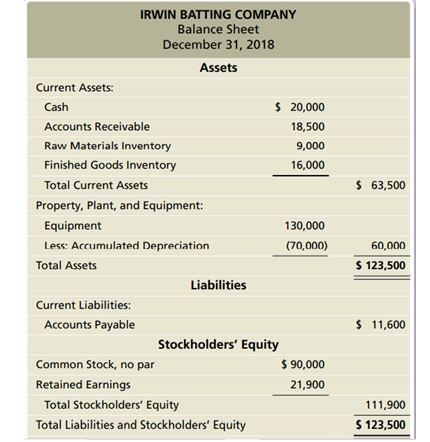

Preparing an operating budget—sales, production, direct materials, direct labor, overhead, COGS, and S&A expense budgets The Irwin Batting Company manufactures wood baseball bats. Irwin’s two primary products are a youth bat, designed for children and young teens, and an adult bat, designed for high school and college-aged players. Irwin sells the bats to sporting goods stores, and all sales are on account. The youth bat sells for \(35; the adult bat sells for \)50. Irwin’s highest sales volume is in the first three months of the year as retailers prepare for the spring baseball season. Irwin’s balance sheet for December 31, 2018, follows:

![]()

Other data for Irwin Batting Company for the first quarter of 2019:

a. Budgeted sales are 1,400 youth bats and 3,300 adult bats.

b. Finished Goods Inventory on December 31, 2018, consists of 700 youth bats at \(15 each and 550 adult bats at \)10 each.

c. Desired ending Finished Goods Inventory is 220 youth bats and 300 adult bats; FIFO inventory costing method is used.

d. Direct materials requirements are 40 ounces of wood for youth bats and 70 ounces of wood for adult bats. The cost of wood is \(0.10 per ounce.

e. Raw Materials Inventory on December 31, 2018, consists of 90,000 ounces of wood at \)0.10 per ounce.

f. Desired ending Raw Materials Inventory is 90,000 ounces (indirect materials are insignificant and not considered for budgeting purposes).

g. Each bat requires 0.4 hours of direct labor; direct labor costs average \(26 per hour.

h. Variable manufacturing overhead is \)0.30 per bat.

i. Fixed manufacturing overhead includes \(1,300 per quarter in depreciation and \)14,977 per quarter for other costs, such as insurance and property taxes.

j. Fixed selling and administrative expenses include \(13,000 per quarter for salaries; \)3,500 per quarter for rent; \(1,400 per quarter for insurance; and \)450 per quarter for depreciation. k. Variable selling and administrative expenses include supplies at 1% of sales.

Requirements

1. Prepare Irwin’s sales budget for the first quarter of 2019.

2. Prepare Irwin’s production budget for the first quarter of 2019.

3. Prepare Irwin’s direct materials, direct labor budget, and manufacturing overhead budget for the first quarter of 2019. Round the predetermined overhead allocation rate to two decimal places. The overhead allocation base is direct labor hours.

4. Prepare Irwin’s cost of goods sold budget for the first quarter of 2019.

5. Prepare Irwin’s selling and administrative expense budget for the first quarter of 2019.