Chapter 6: Q89E (page 367)

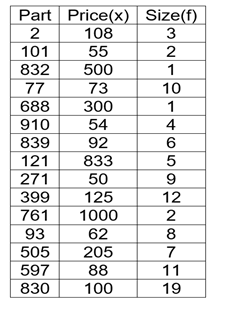

Question: Auditing sampling methods. Traditionally, auditors have relied to a great extent on sampling techniques, rather than 100% audits, to help them test and evaluate the financial records of a client firm. When sampling is used to obtain an estimate of the total dollar value of an account—the account balance—the examination is known as a substantive test (Audit Sampling—AICPA Audit Guide, 2015). In order to evaluate the reasonableness of a firm’s stated total value of its parts inventory, an auditor randomly samples 100 of the total of 500 parts in stock, prices each part, and reports the results shown in the table.

a. Give a point estimate of the mean value of the parts inventory.

b. Find the estimated standard error of the point estimate of part a.

c. Construct an approximate 95% confidence interval for the mean value of the parts inventory.

d. The firm reported a mean parts inventory value of $300. What does your confidence interval of part c suggest about the reasonableness of the firm’s reported figure?

Short Answer

Answer

- The mean value of the parts inventory is 156.46.

- The standard error for the calculated point estimate is 18.7020.

- The 95% confidence interval is (119.0558, 193.8642).

It is observed that the mean parts inventory value of $300 is not included in the confidence interval. So the mean parts inventory value of $300 is not reasonable

Step by step solution

Given information

Given data is as follows

Let n denote the total number of parts in stock that is

The sample size is

(a) Calculating the mean

The mean is calculated using the following formula,

Therefore,

(b) Calculating the standard error

The standard deviation is calculated using the following formula,

Therefore,

Consider,

Here,the finite population correction factor should be included in the standard error calculation

The standard error is obtained by using the following formula

Therefore,

(c) Calculating the 95% confidence interval

The 95% confidence intervals for the population mean by using the following formula,

Therefore,

Hence, the 95% confidence interval is (119.0558, 193.8642).

(d) Interpretation

The 95% confidence interval is (119.0558, 193.8642). Thus, it is observed that the mean parts inventory value of $300 is not included in the confidence interval. So the mean parts inventory value of $300 is not reasonable.

Over 30 million students worldwide already upgrade their learning with 91Ӱ��!