Chapter 12: Q3. (page 497)

A monopolist can produce at a constant average (and marginal) cost of AC = MC = \(5. It faces a market demand curve given by Q = 53 - P.

- Calculate the profit-maximizing price and quantity for this monopolist. Also calculate its profits.

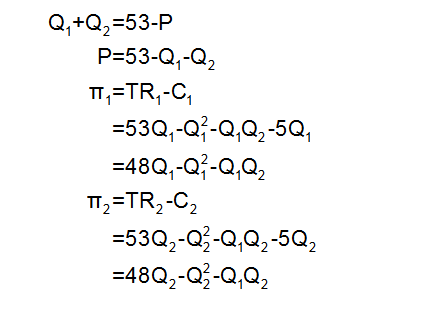

- Suppose a second firm enters the market. Let Q1 be the output of the first firm and Q2 be the output of the second. Market demand is now given by

Q1 + Q2 = 53 - P

Assuming that this second firm has the same costs as the first, write the profits of each firm as functions of Q1 and Q2.

c. Suppose (as in the Cournot model) that each firm chooses its profit maximizing level of output on the assumption that its competitor’s output is fixed. Find each firm’s “reaction curve” (i.e., the rule that gives its desired output in terms of its competitor’s output).

d. Calculate the Cournot equilibrium (i.e., the values of Q1 and Q2 for which each firm is doing as well as it can given its competitor’s output). What are the resulting market price and profits of each firm?

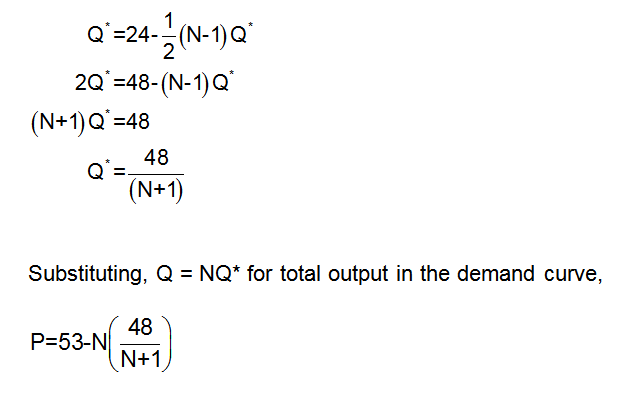

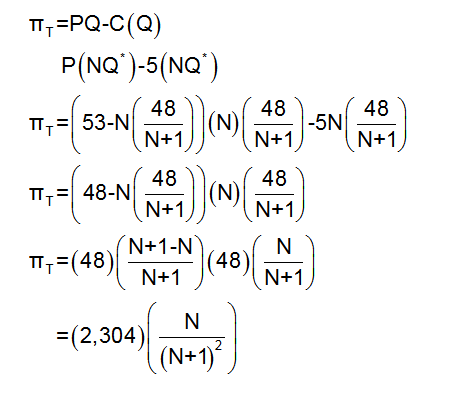

e. Suppose there are N firms in the industry, all with the same constant marginal cost, MC = \)5. Find the Cournot equilibrium. How much will each firm produce, what will be the market price, and how much profit will each firm earn? Also, show that as N becomes large, the market price approaches the price that would prevail under perfect competition.

Short Answer

- The profit-maximizing price will be $29, and the quantity will be 24 units. The profit will be $576.

- The profit for firm 1 will be π1 = 48Q1 – Q12 – Q1Q2, and for firm 2 will be π2 = 48Q2 – Q22 – Q1Q2.

- The reaction curve of firm 1 will be Q1 = 24 – 1/2Q2, and for firm 2 will be Q2 = 24 – 1/2Q1.

- Each firm will produce 16 units at $21. The profit of each firm will be $256.

- Each firm will produce 48 units at $5, and each will earn a zero profit.

Step by step solution

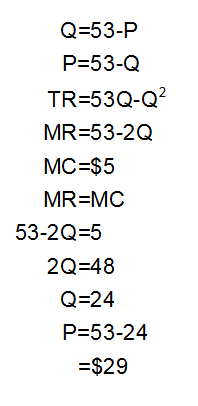

Explanation for part (a)

The monopolist will operate where the marginal revenue is equal to the marginal cost. The price and quantity of the monopolist are calculated below:

The profit-maximizing price will be $29, and the output will be 24 units.

The profit of the monopolist is calculated below:

The profit will be $576.

Explanation for part (b)

After entering a new firm, the market quantity will be the summation of the quantity produced by both firms. The profit function of both the firm is calculated below:

Thus, the profit for firm 1 will be π1 = 48Q1 – Q12 – Q1Q2, and for firm 2 will be π2 = 48Q2 – Q22 – Q1Q2.

Explanation for part (c)

The reaction curve of firm 1 is calculated below:

The reaction curve of firm 2 is calculated below:

Thus, the reaction curve of firm 1 will be Q1 = 24 – 1/2Q2, and for firm 2 will be Q2 = 24 – 1/2Q1.

Explanation for part (d)

From the reaction curves of the firm, the output of each firm is calculated. The output of each firm will be:

The output for each firm will be 16 units.

The price of the market and the profit for each firm is calculated below:

The market price will be $21, and the profit for each will be $256.

Explanation for part (e)

Suppose there are N identical firms; then the market price will be:

P = 53 – (Q1 + Q2+…�Ħ�Ħ�Ħ.

The profit function for ith will be:

Since the cost function is the same, the production level for all firms will be the same; thus, Qi = Q*.

Then the total profit:

The quantity, price, and profit will be if ,

The profit is zero, and the price is equal to marginal cost in perfect competition. The profit is zero, and the price is equal to marginal cost, i.e., $5. Hence, when N approaches infinity, the market approaches perfect competition.

Over 30 million students worldwide already upgrade their learning with 91Ӱ��!