Chapter 11: Q8P. (page 594)

(Comprehensive Fixed-Asset Problem) Darby Sporting Goods Inc. has been experiencing growth in the demand for its products over the last several years. The last two Olympic Games greatly increased the popularity of basketball around the world. As a result, a European sports retailing consortium entered into an agreement with Darby’s Roundball Division to purchase basketballs and other accessories on an increasing basis over the next 5 years.

To be able to meet the quantity commitments of this agreement, Darby had to obtain additional manufacturing capacity. A real estate firm located an available factory in close proximity to Darby’s Roundball manufacturing facility, and Darby agreed to purchase the factory and used machinery from Encino Athletic Equipment Company on October 1, 2016. Renovations were necessary to convert the factory for Darby’s manufacturing use.

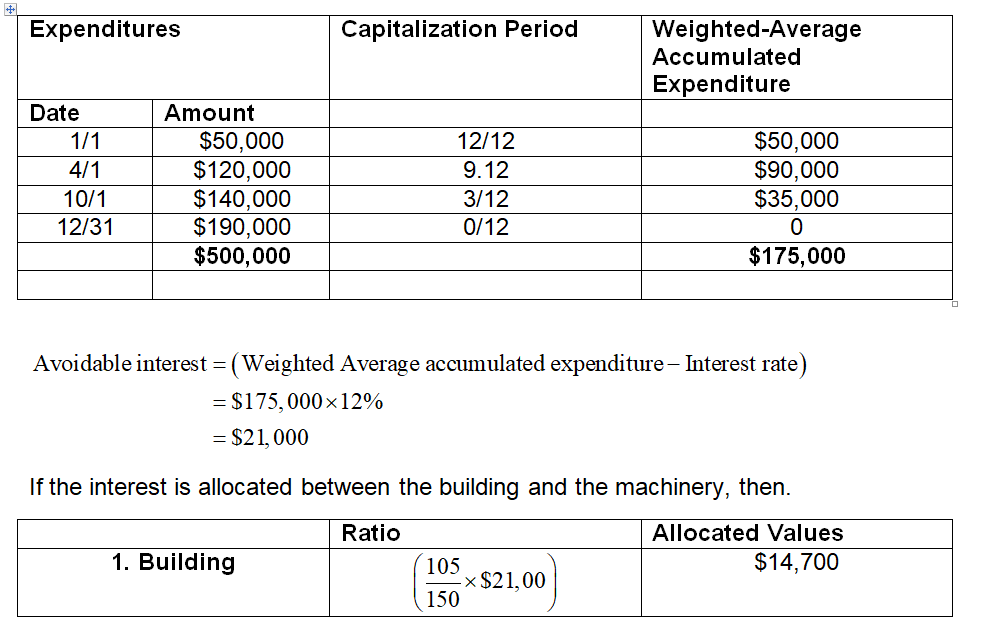

The terms of the agreement required Darby to pay Encino \(50,000 when renovations started on January 1, 2017, with the balance to be paid as renovations were completed. The overall purchase price for the factory and machinery was \)400,000. The building renovations were contracted to Malone Construction at \(100,000. The payments made, as renovations progressed during 2017, are shown below. The factory was placed in service on January 1, 2018.

1/1 | 4/1 | 10/1 | 12/31 | |

Encino | \)50,000 | \(90,000 | \)110,000 | \(150,000 |

Malone | 30,000 | 30,000 | 40,000 |

On January 1, 2017, Darby secured a \)500,000 line-of-credit with a 12% interest rate to finance the purchase cost of the factory and machinery, and the renovation costs. Darby drew down on the line-of-credit to meet the payment schedule shown above; this was Darby’s only outstanding loan during 2017.

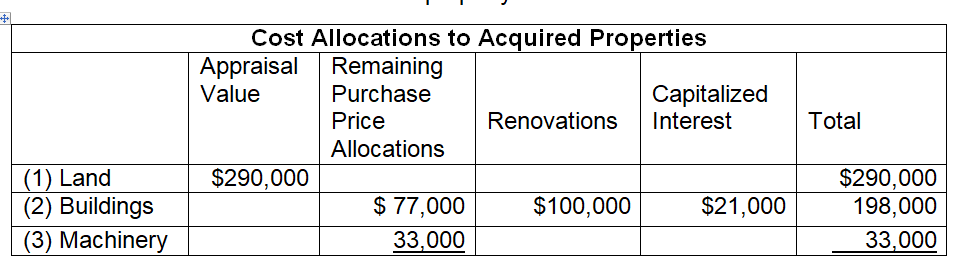

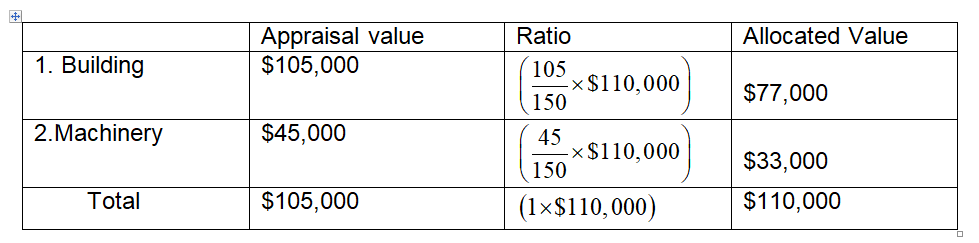

Bob Sprague, Darby’s controller, will capitalize the maximum allowable interest costs for this project. Darby’s policy regarding purchases of this nature is to use the appraisal value of the land for book purposes and prorate the balance of the purchase price over the remaining items. The building had originally cost Encino \(300,000 and had a net book value of \)50,000, while the machinery originally cost \(125,000 and had a net book value of \)40,000 on the date of sale. The land was recorded on Encino’s books at \(40,000. An appraisal, conducted by independent appraisers at the time of acquisition, valued the land at \)290,000, the building at \(105,000, and the machinery at \)45,000.

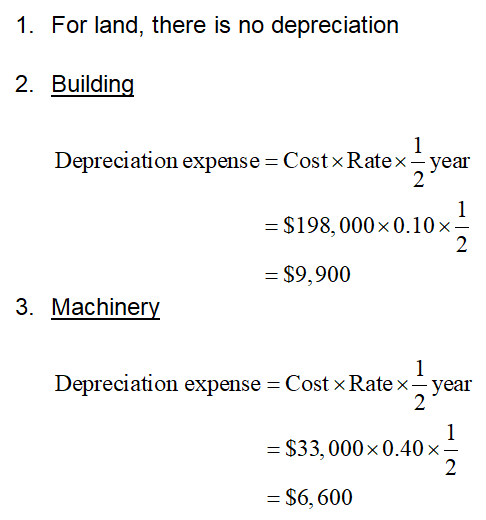

Angie Justice, chief engineer, estimated that the renovated plant would be used for 15 years, with an estimated salvage value of \(30,000. Justice estimated that the productive machinery would have a remaining useful life of 5 years and a salvage value of \)3,000. Darby’s depreciation policy specifies the 200% declining-balance method for machinery and the 150% decliningbalance method for the

plant. One-half year’s depreciation is taken in the year the plant is placed in service, and one-half year is allowed when the property is disposed of or retired. Darby uses a 360-day year for calculating interest costs.

Instructions

- Determine the amounts to be recorded on the books of Darby Sporting Goods Inc. as of December 31, 2017, for each of the following properties acquired from Encino Athletic Equipment Company.

- Land.

- Buildings.

- Machinery.

- Calculate Darby Sporting Goods Inc.’s 2018 depreciation expense, for book purposes, for each of the properties acquired from Encino Athletic Equipment Company.

- Discuss the arguments for and against the capitalization of interest costs.

Short Answer

Land is an asset that is not depreciated over time. The total balance to be allocated is $110,000. Total avoidable interest is $21,000. Diversity of practices among companies and industries called for standardization in practices.

Step by step solution

Meaning of Fixed Asset

In accounting terms, a fixed asset is a tangible asset that is used for more than one year. All fixed assets except land have a tenancy for depreciation on account of obsolescence, and depreciation expense is charged to the books of accounts every year.

(a) Determining the amounts to be recorded on the books of Darby Sporting

The amounts to be recorded for each property is as follows:

Balance of purchase price to be allocated

Working notes:

Calculation of balance to be allocated

(b) Calculating Darby Sporting Goods Inc.’s 2018 depreciation expense

(c) Discussing the arguments for and against the capitalization of interest costs

The following are some of the arguments for capitalizing interest charges.

- The diversity of procedures among enterprises and industries necessitated practice standardization.

- Total interest expenses, like material, labor, and administrative expenditures, should be allocated to firm assets and activities. Any expenses expended to get an asset to the condition and location required for its intended use should be recognized as a cost of that asset under the historical costs approach.

The following are some of the arguments for not capitalizing on interest:

- The amortization of interest capitalized in earlier periods tends to counteract interest accumulated in the current quarter.

- Interest is a finance expense, not a building expense.

Over 30 million students worldwide already upgrade their learning with 91Ӱ��!