Chapter 7: Q7-2FSAC (page 380)

Case 2: Microsoft Corporation

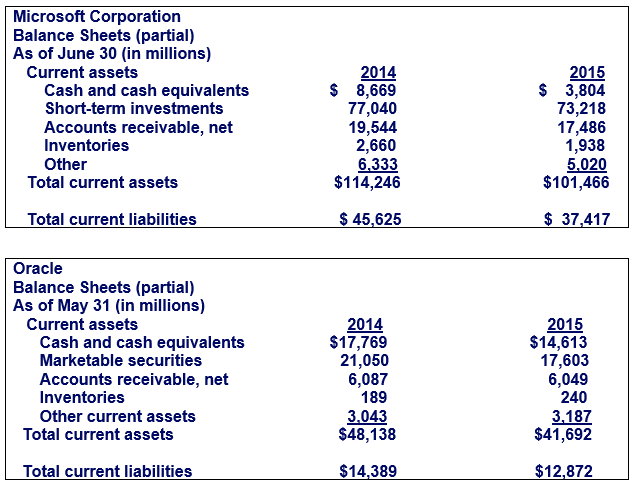

Question: Microsoft is the leading developer of software in the world. To continue to be successful Microsoft must generate new products, which requires significant amounts of cash. The following is the current asset and current liability information from Microsoft’s current balance sheets (in millions). Following the Microsoft data is the current asset and current liability information from

Oracle’s current balance sheets (in millions). Oracle is another major software developer.

Part 1 (Cash and Cash Equivalents)

- Instructions

- What is the definition of a cash equivalent? Give some examples of cash equivalents. How do cash equivalents differ from other types of short-term investments?

- Calculate (1) the current ratio and

(2) working capital for each company for 2014 and discuss your results. - Is it possible to have too many liquid assets?

- Part 2 (Accounts Receivable)

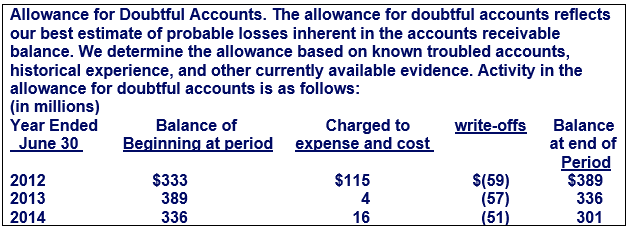

Microsoft provided the following disclosure related to its accounts receivable.

Instructions

- Compute Microsoft’s accounts receivable turnover for 2014 and discuss your results. Microsoft had sales revenue of $69,943 million in 2014.

- Reconstruct the summary journal entries for 2014 based on the information in the disclosure.

- Briefly discuss how the accounting for bad debts affects the analysis in Part 2 (a).

Step by step solution

Over 30 million students worldwide already upgrade their learning with 91Ӱ��!