Chapter 17: Q. 2 (page 469)

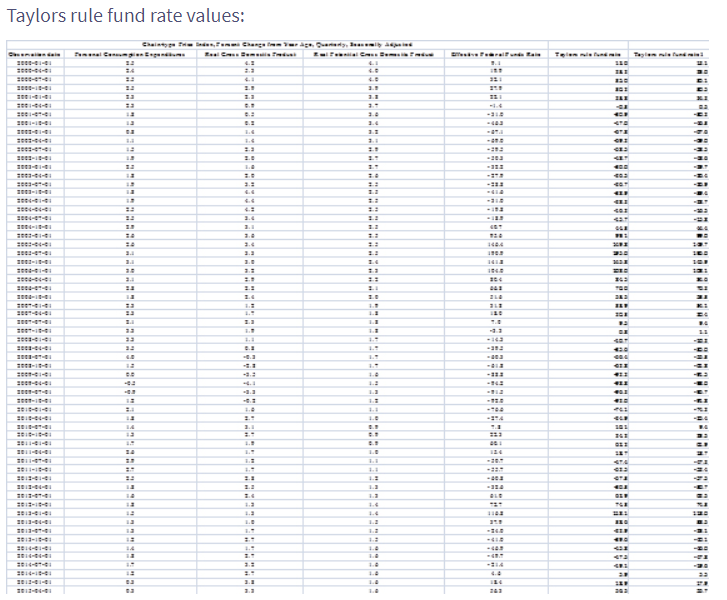

. Go to the St. Louis Federal Reserve FRED database, and find data on the personal consumption expenditure price index (PCECTPI), real GDP (GDPC1), an estimate of potential GDP (GDPPOT), and the federal funds rate (DFF). For the price index, adjust the units setting to “Percent Change From Year Ago” to convert the data to the inflation rate; for the federal funds rate, change the frequency setting to “Quarterly.” Download the data into a spreadsheet. Assuming the inflation target is 2% and the equilibrium real fed funds rate is 2%, calculate the inflation gap and the output gap for each quarter, from 2000 until the most recent quarter of data available. Calculate the output gap as the percentage deviation of output from the potential level of output.

a. Use the output and inflation gaps to calculate, for each quarter, the fed funds rate predicted by the Taylor rule. Assume that the weights on inflation stabilization and output stabilization are both ½ (see the formula in the chapter). Compare the current (quarterly average) federal funds rate to the federal funds rate prescribed by the Taylor rule. Does the Taylor rule accurately predict the current rate? Briefly comment.

b. Create a graph that compares the predicted Taylor rule values with the actual quarterly federal funds rate averages. How well, in general, does the Taylor rule prediction fit the average federal funds rate? Briefly explain.

c. Based on the results from the 2008–2009 period, explain the limitations of the Taylor rule as a formal policy tool. How do these limitations help explain the use of nonconventional monetary policy during this period?

d. Suppose Congress changes the Fed’s mandate to a hierarchical one in which inflation stabilization takes priority over output stabilization. In this context, recalculate the predicted Taylor rule value for each quarter since 2000, assuming that the weight on inflation stabilization is ¾ and the weight on output stabilization is ¼. Create a graph showing the Taylor rule prediction calculated in part (a), the prediction using the new “hierarchical” Taylor rule, and the fed funds rate. How, if at all, does changing the mandate change the predicted policy paths? How would the fed funds rate be affected by a hierarchical mandate? Briefly explain.

e. Assume again equal weights of ½ on inflation and output stabilization, and suppose instead that beginning after the end of 2008, the equilibrium real fed funds rate declines by 0.05 each quarter (i.e. 2009:Q1 is 1.95, then 1.90, etc.), and once it reaches zero, it remains at zero thereafter. How does it affect the prescribed fed funds rate? Why might this be important for policymakers to take into consideration?

Short Answer

(a) The data reveals that Taylor's approach fails to correctly anticipate current fund rates; current fund rates differ from those calculated by Taylor's rule. Personal Consumption Expenditures, Real Gross Domestic Product, Real Potential Gross Domestic Product, and Effective Federal Funds Rate in terms of percent change from a year earlier from 2001:Q1 to 2017:Q4.

(b)

(c) Taylor's rule does not account for all macroeconomic variables that can affect the fund rate (Recession).

(d)

Step by step solution

Step 1. Introduction

John Taylor, a Stanford economist, devised the Taylor's rule formula. It was created to provide "recommendations" on how a central bank, such as the Federal Reserve, should set short-term interest rates when economic conditions change in order to achieve both a short-run goal of economic stabilisation and a long-run goal of inflation.

Step 2. Explanation

The data reveals that Taylor's approach fails to correctly anticipate current fund rates; current fund rates differ from those calculated by Taylor's rule. Personal Consumption Expenditures, Real Gross Domestic Product, Real Potential Gross Domestic Product, and Effective Federal Funds Rate in terms of percent change from a year earlier from 2001:Q1 to 2017:Q4.

The formula for Taylor's rule is as follows:

Targeted Federal Funds Rate

Step 3. (b) Explanation

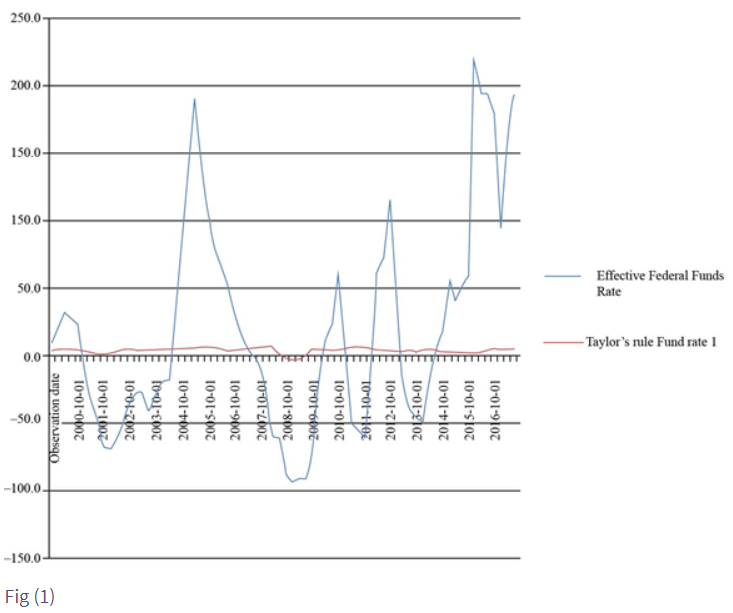

Since 2000, there have been instances when the Taylor rule and the stock market have been fairly tightly connected, particularly from 2000 to 2002 (1). However, there are major gaps at other times (1), or periods where they do not appear to be moving in lockstep (1), such as the period from 2002 to 2006 (1). 4 From 2008 onwards, there are significant differences between the two (1), particularly from late 2008 to early 2010, when the Taylor rule predicts that the federal funds rate should be negative by nearly 4% (1), which is not possible (1). 6 It also forecasted big increases in the federal funds rate in 2011:Q2 (1) and 2014:Q1 (1), both of which did not occur (1). However, the rise in the Taylor rule target in 2016:Q1 indicated a 50 basis point increase in the fed funds rate (1), and the FOMC followed through with two fed funds rate hikes in the first half of 2017 (1) in line with this delta (1).

Step 4. (c) Introduction

The central bank employs monetary policy to control the flow of money into and out of the economy in order to restore stability; this is accomplished through interest rate and money supply management.

Step 5. Explanation

The current fund rate (% change from a year ago) was negative in 2008-09 (the recession period), but the Taylor's rule value was positive. This implies that there are other factors (Recession) that affect the fund rate, and the reason for the incorrect calculation is because Taylor's rule does not account for all macroeconomic variables that can affect the fund rate (Recession).

Taylor's rule's incorrect assessment of the fund rate shows that in this circumstance, nonconventional monetary policy would be the best option.

Step 6. (d) Explanation

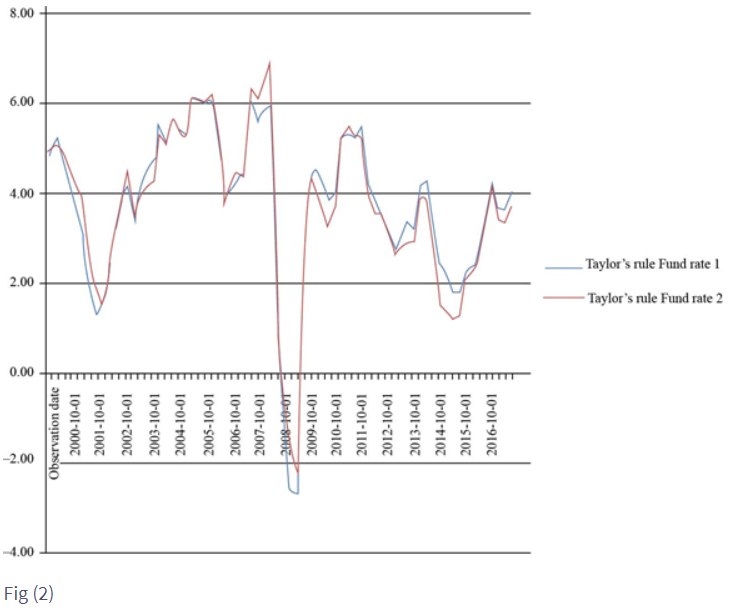

The baseline Taylor rule and the hierarchical Taylor rule forecast almost identical federal funds rate courses for the most part. The only noteworthy shift is from 2008 onwards, when it anticipates a much higher federal funds rate due to the surge in inflation during that time period. The graph below illustrates this:

Step 7. Explanation

Over 30 million students worldwide already upgrade their learning with 91Ӱ��!