Chapter 8: Q3. (page 325)

Use the same information as in Exercise 1.

a. Derive the firm’s short-run supply curve. (Hint:You may want to plot the appropriate cost curves.)

b. If 100 identical firms are in the market, what is the industry supply curve?

Short Answer

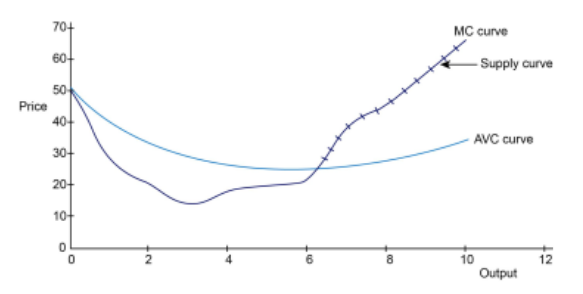

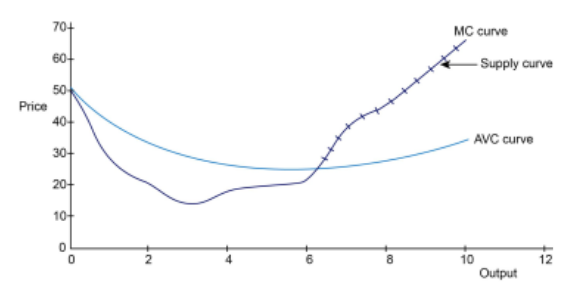

a. The MC curve below above the minimum AVC curve is the short-run supply curve:

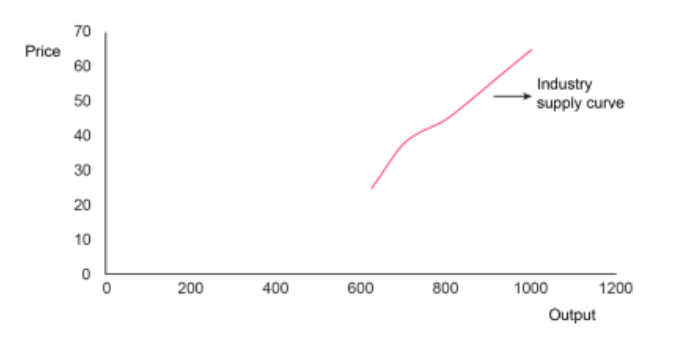

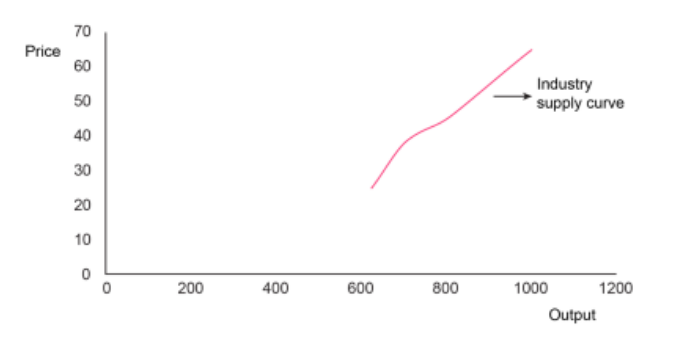

b. The industrial supply curve is given below:

Step by step solution

Deriving the firm’s short-run supply curve

The supply curve tells about the quantity of output supplied for each possible price. A perfectively competitive firm will produce output from the point where the marginal cost starts covering the average variable cost.

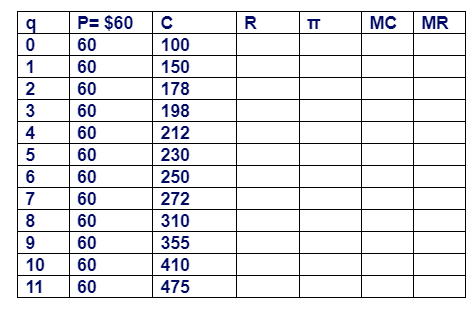

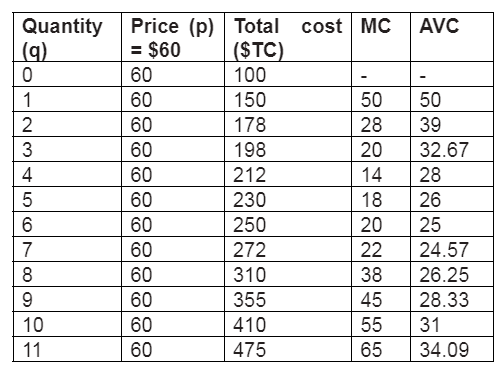

The following data represents the marginal cost and average variable cost of the firm for each price level.

Plotting the marginal cost and average variable costs of the firm for each price level, one can derive the firm’s supply curve.

In the above graph, the part of the marginal curve that lies above the average variable cost (AVC) curve represents the firm’s supply curve. The firm will not produce for the range of price level, which lies below the average variable cost.

Thus, the hatched section of the marginal cost curve represents the supply curve of the firm.

Determining the industry supply curve

Since all firms in the industry are identical, the industry supply curve would be the summation of supply curves of individual supply curves.

The industry supply curve is drawn below for each price level:

Thus, the shape of the industry’s supply curve will be the same as the supply curve of an individual firm. But the number of output produced will be the sum of output produced by 100 firms.

Over 30 million students worldwide already upgrade their learning with 91Ӱ��!