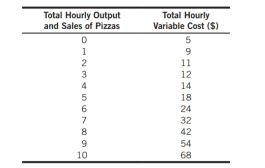

The table nearby represents the hourly output and cost structure for a local pizza shop. The market is perfectly competitive, and the market price of a pizza in the area is . Total costs include all opportunity costs. Fixed costs equal zero.

a. Calculate the total revenue and total economic profit for this pizza shop at each rate of output.

b. Assuming that the pizza shop always produces and sells at least one pizza per hour, does this appear to be a situation of short-run or long-run equilibrium?

c. Calculate the pizza shop's marginal cost and marginal revenue at each rate of output. Based on marginal analysis, what is the profit maximizing rate of output for the pizza shop?

d. Draw a diagram depicting the short-run marginal revenue and marginal cost curves for this pizza shop, and illustrate the determination of its profit-maximizing output rate.