Chapter 25: Q. 7 (page 575)

Suppose that after long-run adjustments take place in the used-book market, the business in Problem ends up producing units of output. What are the market price and economic profits of this monopolistic competitor in the long run?

Short Answer

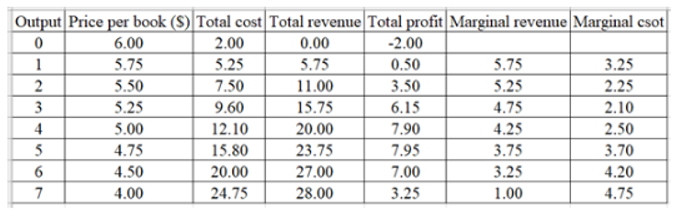

The Market price is and the economic profit is when the firm producing four units.

Step by step solution

Introduction.

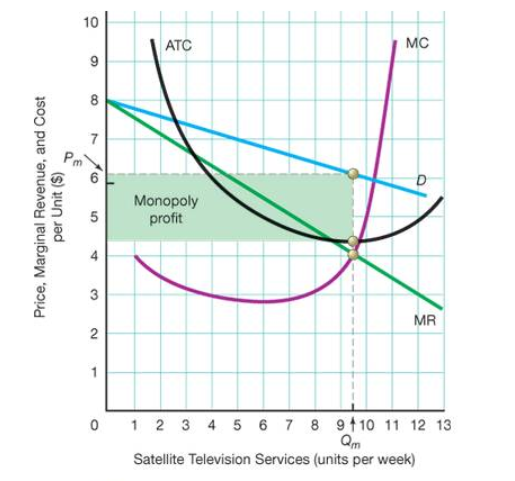

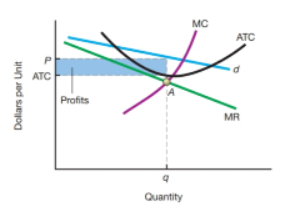

The monopolistic competitor will instead produce at just that level and charge the price suggested by the demand curve for the company's product.

If firms in a monopolistic competitive industry make economic profits, the industry will attract new applicants until, in the long run, profits are reduced to zero.

Given Information.

- With an imperfect market structure and a high number of buyers and sellers, a monopolistically competitive market exists. In this market system, different items are offered by different sellers.

- For a monopolistically competitive corporation, such as a monopoly market, the profit-maximizing condition is marginal revenue equal to marginal cost.

Table explanation.

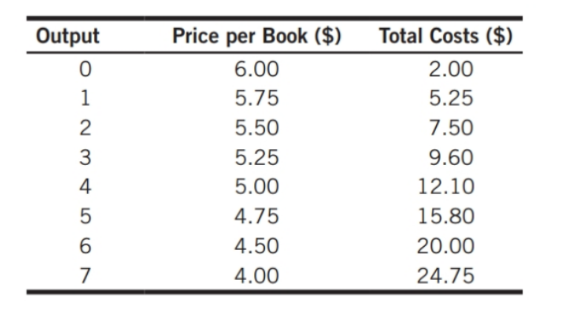

The following table shows the total revenue, marginal revenue, and marginal cost for the book store from the previous question:

Market price.

- The company will choose the quantity in which the contribution margin above or equals the marginal cost in the near term.

- Determine the market cost that is related to the equilibrium quantity using the demand curve.

- The average cost of manufacturing finally matches the market price. When the market price equals the average total cost, economic profits are zero.

Find the market price and economic profits.

After long-run modifications, the factory creates four units of output. At this level of output, the average total cost is

As a result, the market price is , while the economic profit is .

Over 30 million students worldwide already upgrade their learning with 91Ӱ��!