Chapter 25: Q. 2 (page 575)

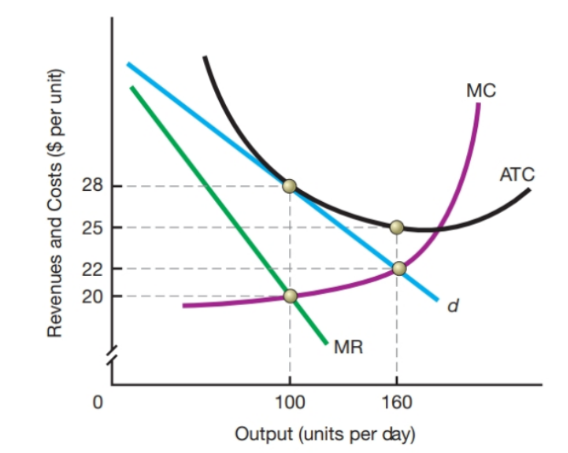

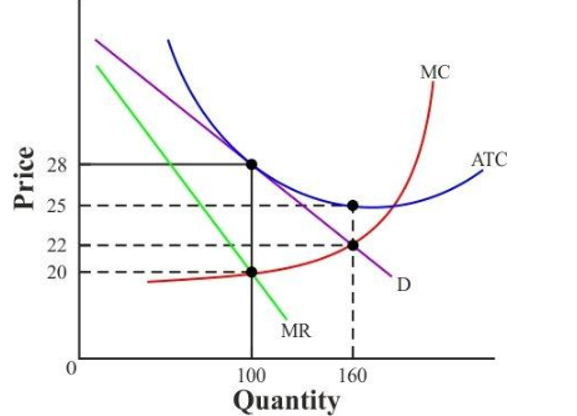

Consider the diagram nearby depicting the demand and cost conditions faced by a monopolistically competitive firm.

a. What are the total revenues, total costs, and economic profits experienced by this firm?

b. Is this firm more likely in short- or long-run equilibrium? Explain.

Short Answer

(a) Total Revenue is , Total cost is and Economic profit is

(b) The firm makes a profit in the short run, but no economic profit in the long run. As a result, the company has reached long-run equilibrium.

Step by step solution

Introduction.

- Monopolistic competition depicts a market in which a large number of companies provide similar (but not ideal) replacements for their products or services.

- In a monopolistic competitive industry, entrance and exit barriers are minimal, and one firm's choices have little influence on its competitors.

Given Information (part a).

The diagram below depicts the total output, revenue, and cost of a monopolistically competitive firm:

The -axis in the diagram above represents quantity, and the -axis represents cost. The marginal product curve is cut by the marginal cost curve from below. The average variable cost curve is shaped like a .

Profit Maximizing Output (part a).

The profit-maximizing output is determined when the marginal revenue equals the marginal cost. The demand curve indicates the output price.

The Economic Profit (part a).

There are two profit-maximizing outputs in the diagram. As a matter of fact, we will look into both possibilities.

If the quantity is units per day. Therefore, the price is .

Total revenue

localid="1652253673696"

Total cost

Total revenue minus total costs equals economic profit.,

Hence, it is .

Find the firm is in short- or long-run equilibrium (part b).

In the shorter term, the firm makes a profit, but in the long run, the firm makes no economic profit. The firm earns no economic profit in the given situation. As a result, the firm is in long-run equilibrium.

Over 30 million students worldwide already upgrade their learning with 91Ӱ��!